ALBANY INTERNATIONAL CORP /DE/ (AIN)·Q4 2025 Earnings Summary

Albany International Revenue Beats by 10% as Engineered Composites Surges 43%

February 24, 2026 · by Fintool AI Agent

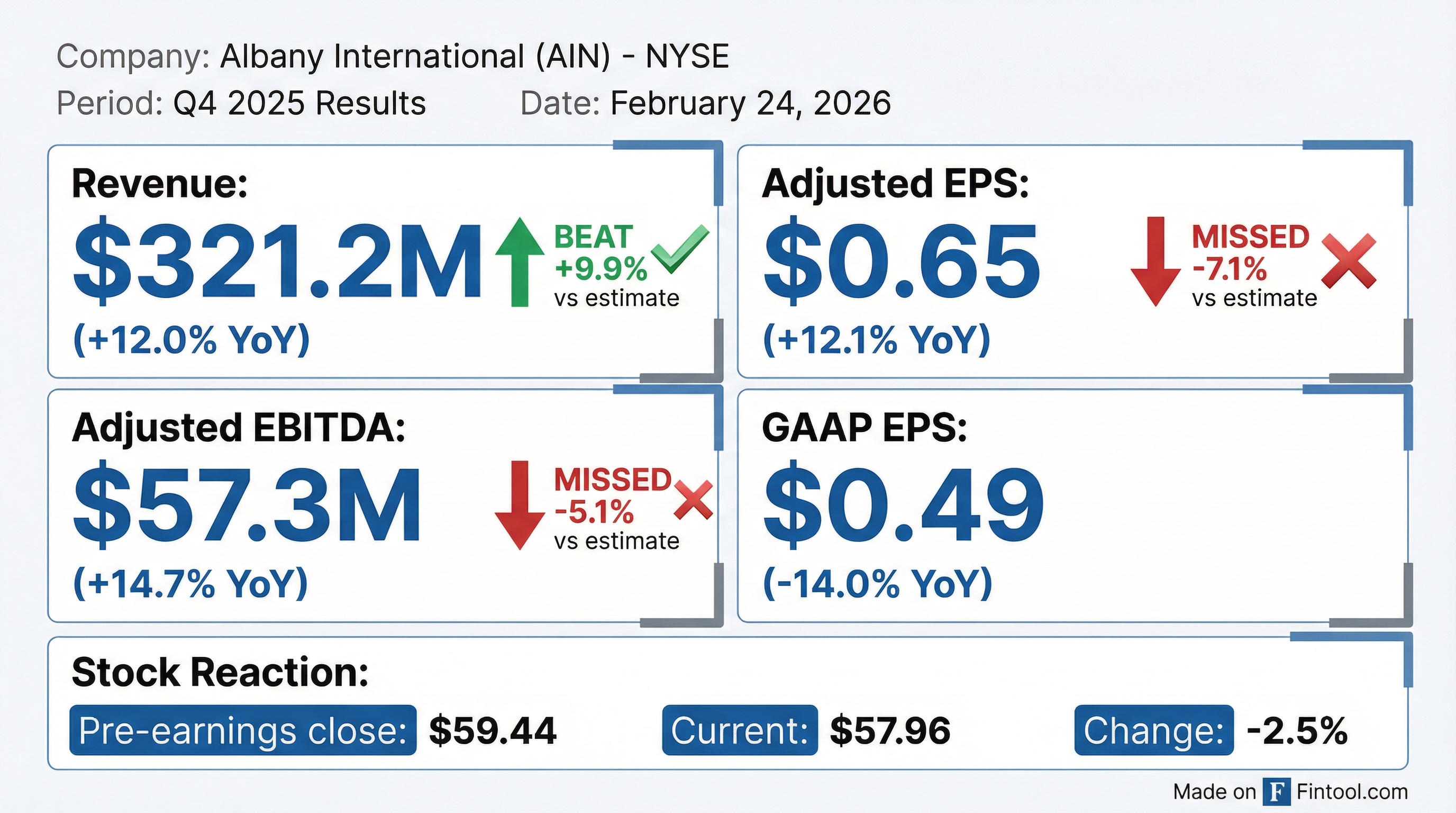

Albany International (NYSE: AIN) delivered a mixed Q4 2025, with revenue beating estimates by nearly 10% on strength in Engineered Composites, while adjusted EPS missed consensus by 7% due to an elevated tax rate. The company announced a strategic review of its structures assembly business, signaling a portfolio sharpening that management says will focus resources on higher-return opportunities.

Did Albany International Beat Earnings?

Revenue beat, EPS missed. Albany posted Q4 2025 revenue of $321.2 million, beating consensus of $292.3 million by 9.9%. However, adjusted EPS of $0.65 missed the $0.70 estimate by 7.1%. GAAP EPS was $0.49, down from $0.57 in Q4 2024.

The EPS miss was driven primarily by a 39.3% effective tax rate in Q4 2025, compared to 28.0% in Q4 2024. Management attributed this to the expiration of a foreign tax credit and less favorable discrete tax adjustments.

What Changed From Last Quarter?

Strategic portfolio sharpening. The biggest news was the announcement of a strategic review of the structures assembly business and its Salt Lake City production site. Albany has engaged an advisor to help guide the transaction.

CEO Gunnar Kleveland framed the move as focusing on core competitive advantages:

"This action will position the remaining Aerospace portfolio to align more closely with our strategic priorities and to pursue growth opportunities where our differentiated technologies provide a clear competitive advantage and stronger returns."

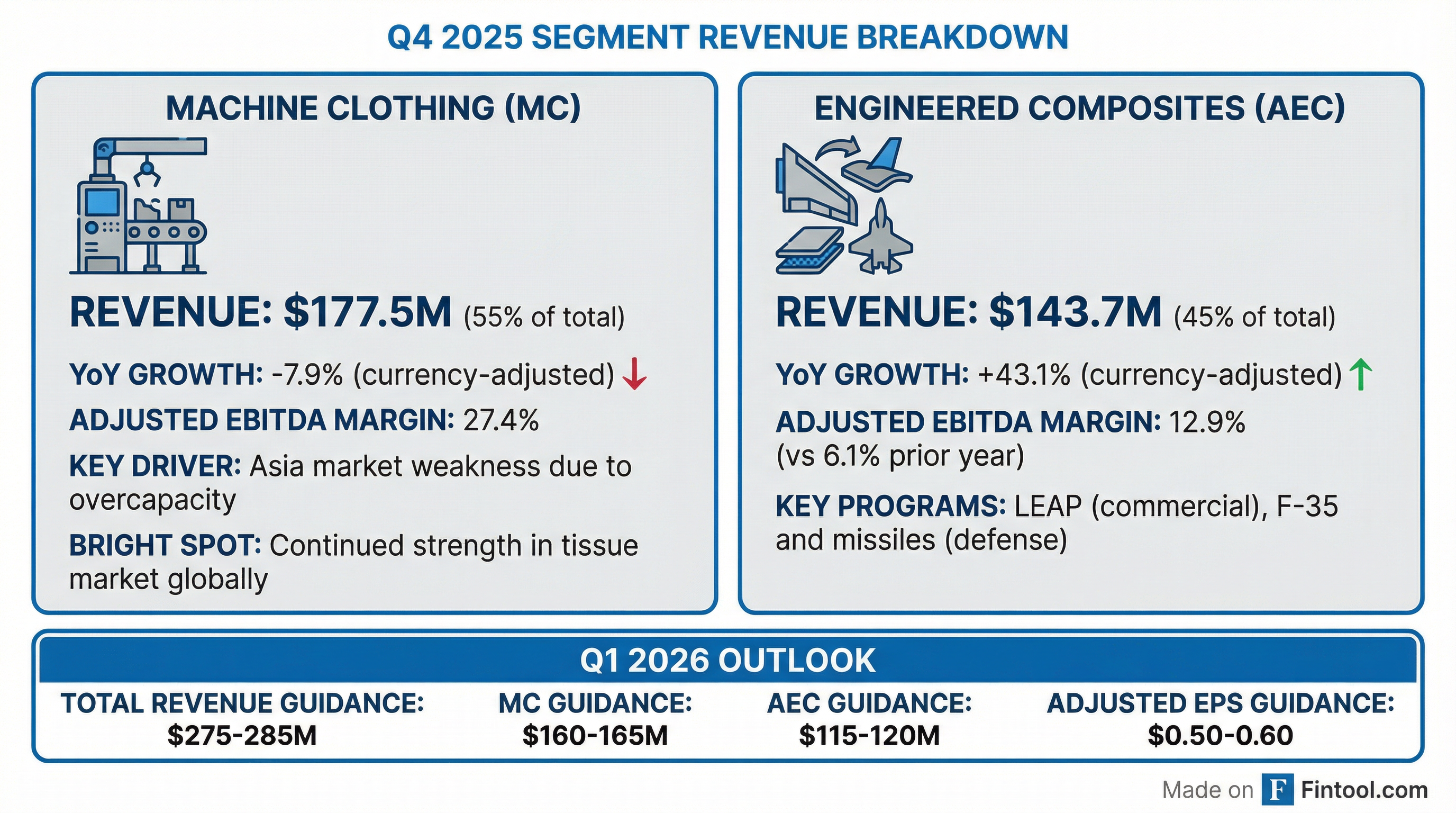

Segment divergence continued. The two business segments moved in opposite directions:

-

Engineered Composites (AEC) surged 43.1% YoY (currency-adjusted), driven by LEAP program commercial ramp and F-35/missile defense programs. Adjusted EBITDA margin improved dramatically to 12.9% from 6.1%. Management highlighted BETA certification underway with production ramping, Bell 525 successfully completing development, and LEAP expected to deliver double-digit growth over the next couple of years.

-

Machine Clothing (MC) declined 7.9% YoY (currency-adjusted) due to weakness in Asia markets from overcapacity, though tissue markets remained strong globally. Margin contracted to 27.4% from 28.5%. Management noted China weakness showed "no further deceleration since Q3," while Americas growth in tissue was partly offset by industry consolidation in packaging/corrugator. Europe has stabilized with consistent H2 demand.

What Did Management Guide?

Q1 2026 guidance below Q4 run rate. Albany provided the following outlook:

Equipment failure to impact Q1 EPS by $0.10-0.15. Machine Clothing's Americas segment is being impacted by an equipment failure at a North American facility, which will have a $0.10 to $0.15 EPS impact in Q1. Management expects to recover this impact over the course of the year.

The sequential revenue decline reflects normal seasonality, but the normalization of the tax rate to 27% and recovery from the equipment issue should provide EPS tailwinds later in 2026.

How Did the Stock React?

Down 2.5% on the day. AIN shares fell from $59.44 to $57.96, declining 2.5% following the earnings release. The stock remains well off its 52-week high of $81.03.

The negative reaction likely reflects the EPS miss and below-expectation Q1 guidance, offsetting the revenue beat.

Capital Allocation Update

Albany continued its balanced capital allocation approach:

Balance sheet remains solid:

- Cash and equivalents: $112.4M

- Total debt: $455.7M

- Net debt: $343.3M

- Net Leverage Ratio: 1.7x

CFO Will Station emphasized the focus on returns:

"Over the past 6 months, we have sharpened our strategy to focus more squarely on our core competitive advantages... That focus is guiding how we operate the business and how we allocate capital, with a clear objective of investing where we can generate attractive returns and maximize long-term value for shareholders."

Full Year 2025 Review

The full year was marred by a Q3 2025 CH-53 contract loss provision of $139.7M, which drove a GAAP net loss of $57.0M for the year.

Key Takeaways

-

AEC is the growth engine: Engineered Composites delivered 43% revenue growth and dramatically improved margins. LEAP expected to deliver double-digit growth over the next couple years, with BETA certification and Bell 525 development progressing.

-

MC under pressure, but stabilizing: Machine Clothing faces structural headwinds in Asia, though management noted "no further deceleration since Q3" in China. Tissue remains a bright spot globally.

-

Portfolio simplification coming: The strategic review of the structures assembly business signals Albany is exiting lower-return assets to focus on differentiated technologies.

-

Q1 headwinds are temporary: Equipment failure will impact Q1 EPS by $0.10-0.15, but recovery expected during the year. Tax rate normalizes to 27% from Q4's 39.3%.

-

Balance sheet supports flexibility: Net leverage of 1.7x, $112M cash, and $81M FY25 FCF enable continued buybacks (repurchased 10% of shares in 2025) and dividends.

Q&A Highlights

Ceramic Matrix Composites (CMC) — New Growth Initiative

CEO Gunnar Kleveland revealed details on Albany's emerging Ceramic Matrix Composites (CMC) business for the first time:

"We have been investing in high-temperature composites using our proprietary 3D weaving then carbonizing those near-net shape parts. We've been working with several OEMs. In Rochester, we now have the full capability to make carbon-carbon and various Ceramic Matrix Composites."

Key points:

- Near-net shape manufacturing reduces expensive machining of carbon materials

- Applications span hypersonic missiles to nozzles and exhausts on traditional missiles

- Positioned as "a strong growth engine for R&D in the short term and as part of production in the short to medium term, definitely in the longer term"

Salt Lake City Strategic Review Update

Management provided an update on the Amelia Earhart facility divestiture process:

- Guggenheim retained as advisor to guide the process

- Interest from both private equity and strategics — autoclave capacity is "very attractive"

- More announcements expected "throughout the spring"

- Site performing well and aligned with Sikorsky on deliveries

LEAP Program and AEC Margins

CFO Will Station provided specific metrics on key programs:

- LEAP volume up 27% YoY — factory fully operating and supporting OEM ramps, "completely aligned" with GE's 15% delivery increase targets

- CH-53K fully resolved — losses covered by Q3 charge, no further charges expected

- AEC margin targets: 10% overall while Salt Lake is included; targeting mid-to-low teens after strategic review completion

Other Notable Q&A Points

- Equipment failure resolved — Machine Clothing equipment failure at the North American facility has been restored and is operating; team closely monitoring

- Corporate relocation complete — Albany moved headquarters to Portsmouth, NH, positioning to attract talent "across a broad and highly skilled corridor stretching from Boston to Portland"

- European exits — Part of Heimbach synergies, exiting low-margin businesses and optimizing the network

Data sources: Albany International 8-K filed February 24, 2026; Albany International Q4 2025 Earnings Call Transcript; S&P Global consensus estimates; market data as of February 24, 2026.